Commentary

By burying disagreements in imprecision, the new deal risks same fate as its predecessors.

James M. Acton

{

"authors": [

"Helima Croft",

"Aaron David Miller"

],

"type": "commentary",

"blog": "Emissary",

"centerAffiliationAll": "dc",

"centers": [

"Carnegie Endowment for International Peace"

],

"englishNewsletterAll": "americanStatecraft",

"nonEnglishNewsletterAll": "",

"primaryCenter": "Carnegie Endowment for International Peace",

"programAffiliation": "ASP",

"programs": [

"American Statecraft"

],

"regions": [

"Middle East",

"Iran",

"Europe",

"United States"

],

"topics": [

"Energy",

"Trade",

"Domestic Politics",

"Foreign Policy"

]

}

Photo by Samuel Boivin/NurPhoto via Getty Images

Why the Iran ceasefire isn’t a quick fix to the Strait of Hormuz energy crisis.

On Tuesday’s episode of Carnegie Connects, hours before the Iran ceasefire took effect, Aaron David Miller spoke with Helima Croft, head of global commodity strategy and MENA research at RBC Capital Markets. Excerpts from their conversation, which have been edited for clarity, are below.

Aaron David Miller: Helima, I remember our conversation in June 2022, several months after Russia’s invasion of Ukraine, when we were dealing with what seemed to be a major oil crisis.

Helima Croft: In that conflict, we were talking about 3 million barrels a day potentially coming off the market. That sent Brent [crude] prices to around $128. Now, we’re dealing with an actual physical disruption of 10 million–plus barrel a day. We have Brent prices at this moment at around $110. This is the biggest energy supply [shock] that we’ve seen in history.

Aaron David Miller: What domestic policies are or are not available to compensate for the shortage?

Helima Croft: On any given day, about 17 million barrels move through [the Strait of Hormuz]. But we’re probably talking about a disruption of around 10 million or 11 million barrels, because the Saudis have been able to use the East-West Pipeline. That pipeline has a capacity of 7 million, but the export component of that is about 5 million.

They run it to the port in Yanbu, the Red Sea port, which has been exporting about 4.5 million barrels. So it’s a partial offset, but nowhere near compensating for the volumes that have been lost and physical fields shut down because a number of these producer states have reached what we call tank tops, where you can’t store anymore.

We’re quickly running through the available shock absorbers. Shock absorber number one is strategic reserves. [In 2022 after Russia invaded Ukraine] the United States released 180 million barrels of oil from our strategic petroleum reserve, the largest release we’ve ever done, and we’ve never refilled. Now we’ve announced another 172 million, and once that is exhausted, we’re down to very low levels. Other countries have stockpiled as well, but multiply 10 million times 30 days, and that wipes out basically the remaining reserves.

Aaron David Miller: The International Energy Agency published a list of suggestions about reducing demand, including reducing your highway speed by 10 miles per hour, using public transportation, avoiding air travel if possible.

Helima Croft: Asian countries are already doing that. If you look at Malaysia, Pakistan, Vietnam—they’re implementing forms of rationing and work-from-home policies.

That’s starting to migrate to Europe. In Italy, jet fuel is [an issue]—we’re going to start to really see this in Europe as we progress in this crisis. The UK [imports] Qatari gas, but there is no offset [like the East-West Pipeline for Saudi oil] for Qatari LNG. And we’ve already had reports that Ras Laffan, the world’s largest LNG facility, has been significantly damaged.

Europe made the decision to go off of Russian hydrocarbons [due to the war in Ukraine]. And who was an important backfill? Qatar. They rerouted supplies that were not needed for Asia because of warmer weather to Europe. So if we really have a significant and prolonged outage of Qatari LNG, that’s going to be a factor as we get into winter.

We’re going to start [seeing] the effects beyond Asia soon. And you have the United States’s summer driving season. We’re going to be facing, I think, significantly higher prices come summer. And remember, it’s a globally traded product.

Aaron David Miller: Plus, fertilizer prices have gone up 20 to 30 percent. Then there’s helium . . .

Helima Croft: I think people almost don’t want to come to grips with the severity of this economic shock. We’re still in a period of irrational optimism that it will end soon, because people can’t wrap their heads around what this looks like going into summer.

Invalid video URL

Aaron David Miller: I’m a rock-and-roller, so let’s move on to the dire straits problem.

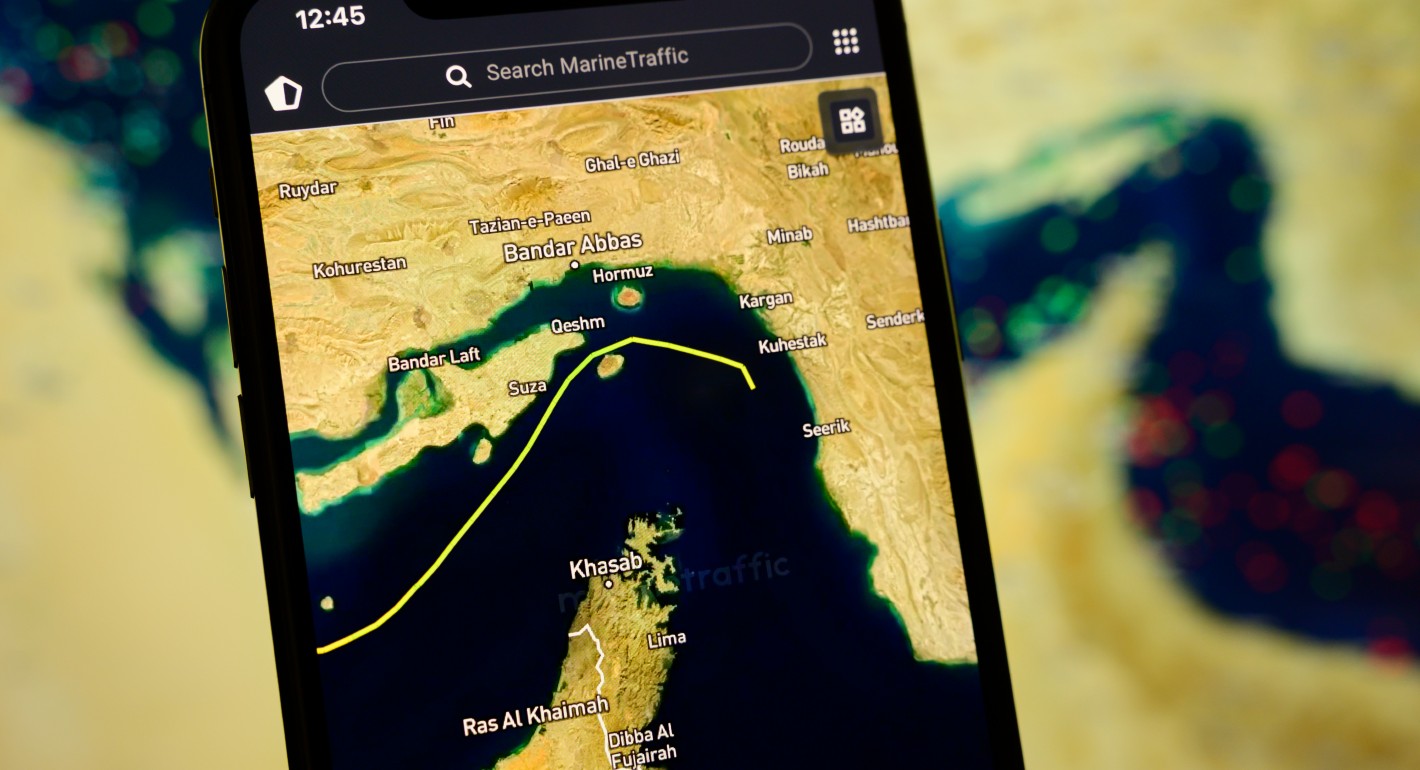

A putative search for a nuclear weapon is no longer what provides the Iranians with leverage and the focal point of the conversations. It’s now geography as destiny. Talk to us about the Strait of Hormuz.

Helima Croft: I think what is so interesting is that the Iranians have not had to deploy their navy to close the Strait of Hormuz. They have been able, through drone and missile attacks around the waterway, to effectively convince shippers and insurers that it is not safe to traverse the strait.

I think what we did not anticipate is the ease with which Iran could essentially change risk calculations of a variety of entities. The question now is: What is it going to take to get these same entities to feel OK going through there?

What really worried me early on was when [Kuwait Petroleum Corporation CEO] Sheik Nawaf Al-Sabah, in an interview in Princeton Alumni Weekly of all places, said, look, we’re not going to have our tanker fleet move around the Middle East unless we get very serious guarantees that it is safe to do so. What type of end game gives confidence that these waters are safe? When you hear certain Gulf state leaders say that we have to ensure that Iran is not operating a tollbooth, that they’re not controlling the waterways, how do we get to the point? What does that entail? How do we end up with Iran not in control of the strait?

Aaron David Miller: One option is regime change, or a compliant regime that’s willing to cooperate.

Helima Croft: Or you have to get a deal done . . .

Aaron David Miller: Even if you came up with a plan to disengage, you’d still be left with a significant shortage. It’s not like turning a switch on and off to restore 20 percent of global oil needs the day after it comes to an end.

Helima Croft: The Achilles’ heel is storage. One of the warning signs that this conflict was probably going to be much more disruptive than most people realized was how quickly countries moved to physically shutting in fields. We were shutting in production within days of the start of the conflict. Iraq is OPEC’s second largest producer, and it is dependent on the port in Basra to move its exports. But when you can’t export, you run through storage. When storage reaches “tank tops,” you physically have to shut in fields. And Iraq was one of the first to have to start physically shutting in large amounts of production.

Then you have to think about the restart time. Sheik Nawaf said that Kuwait would probably take three to four months for full return of production—and Kuwait’s national oil company is a very well-run and resourced [operation]. Then you think about Iraq, which has significant infrastructure problems. Part of the reason why Iraqi exports have not been higher is the lack of investment in pipelines and port infrastructure and storage—all the enabling infrastructure that you need to be a massive exporter. So the restart time in Iraq [will likely] lag Kuwait.

So the idea that we’re going to have significant volumes coming back on day one—even if this conflict ends and Iran says everyone can go through, [we may see] prolonged outages. I don’t think market participants are really taking that on board. I think there’s a corner of the market that thinks this ends, everybody goes through, and those fields are back up and running in a couple of weeks.

The latest from Carnegie scholars on the world’s most pressing challenges, delivered to your inbox.

Aaron David Miller: Six weeks in, is it possible to identify winners and losers?

Helima Croft: I would say at top of the list is Vladimir Putin. The United States at the end of 2025 had made the decision to finally impose significant blocking sanctions on Russia’s two largest oil producers. Now, Russian oil is effectively part of our strategic reserves that we’re tapping. Those Russian barrels can now move to India or China. And the Russians can say, “We’re not accepting a discount anymore. This is a premium-grade product,” and the Russian ATM gets refilled.

Also, I think China is an interesting watch, because China prepared in advance for this. Part of the reason why we did not have Brent prices in the $40s and $50s in 2025, despite all the conversation about being oversupplied, is that China had been aggressively buying for its strategic reserves. They had been building out storage. When you talk to senior Trump administration officials, they fully concede that China was buying for strategic reasons, not commercial. They were basically hedging against Middle East supply disruption, which proved to be a very smart decision, and also potentially preparing for conflict with the United States. So I think China has more bandwidth to endure an outage from the Middle East.

From Iran’s standpoint, it obviously has suffered massive blows to leadership and infrastructure. But from a financial standpoint, at least when it comes to oil revenue, the fact that [the United States] removed sanctions from Iran . . . to me, it’s paradoxical that we are bombing a country but also allowing them to sell their oil unsanctioned.

Aaron David Miller: I think the losers are pretty evident. The Europeans seem to be in really bad shape.

Helima Croft: The Europeans made the decision to basically cease importing Russian hydrocarbons in large quantities and [replace it with] seaborne oil, which is now essentially off the market. And Trump is again threatening to pull out of NATO, saying that security is Europe’s responsibility. But the European countries don’t want to become involved in military operations for a war they did not start. So I think Europe has really been once again left holding the bag.

Aaron David Miller: And then you have the civilians who are caught up in this conflict, including the Iranian people. . . .

I want to ask you a big picture question about the future: the end of oil. Wouldn’t you think that in a rational world—not tethered to a galaxy far, far away—that for reasons of energy security alone, there would be a now, that we’ve reached some sort of tipping point?

Helima Croft: I think we’re going to see a variety of policy responses. I think in Europe we’ll end up in an “all of the above.” China has already been doing all of the above. The Chinese are already heavily investing in solar, hydro—basically saying we need it all because we want to win the AI race. Europe may once again have conversations about the optical energy mix, so that they’re not dependent on single suppliers. For the United States, given our resource endowment and as long as we have this administration, the focus will be on permitting reform, “drill, baby, drill,” basically building out all the pipelines necessary.

But if we think about the oil shocks of the ’70s, what we do see is an emphasis on building strategic reserves. We’re going to see countries deciding that they need to have bigger shock absorbers, building out more energy storage—maybe building storage closer to consumer markets as well. I do think there’s going to be an emphasis on that type of infrastructure investment going forward.

Listen to the full episode and subscribe to Carnegie Connects here.

Helima Croft

Managing Director, Head of Global Commodity Strategy and MENA Research, RBC Capital Markets

Helima Croft is a managing director and the head of Global Commodity Strategy and Middle East and North Africa (MENA) research at RBC Capital Markets. She specializes in geopolitics and energy, leading a team of commodity strategists that cover energy, metals, and cross‐commodity investor activity.

Senior Fellow, American Statecraft Program

Aaron David Miller is a senior fellow at the Carnegie Endowment for International Peace, focusing on U.S. foreign policy.

Carnegie does not take institutional positions on public policy issues; the views represented herein are those of the author(s) and do not necessarily reflect the views of Carnegie, its staff, or its trustees.

By burying disagreements in imprecision, the new deal risks same fate as its predecessors.

James M. Acton

The United States and Israel may have unwittingly revived the Islamic Republic’s “zombie regime.”

Suzanne Maloney, Aaron David Miller, Karim Sadjadpour

The Islamic Republic’s words and actions suggest that it has changed its approach to both diplomacy and war.

Mohammad Ayatollahi Tabaar

Why the outcomes of the U.S.-China meetings may be limited.

Aaron David Miller, David Rennie

Instead, governments should adopt climate-friendly measures to address the impact of rising prices.

Henok Asmelash